As more Indians participate in a widening range of investments, from financial instruments to property, the question of how gains are taxed is becoming increasingly relevant to middle-class taxpayers too. Whether it is selling shares after a market rally, redeeming mutual fund units, or transferring a house or plot of land, long-term capital gains or LTCG, tax now touches far more people than it once did.What was earlier seen as a concern mainly for seasoned investors or large asset holders is turning into a middle-class compliance issue. With rising retail participation in markets and continued activity in real estate, many taxpayers are finding that understanding how long an asset must be held, what tax rate applies, and how gains can be adjusted against losses is not always straightforward.

Against this backdrop, and with the Union Budget just around the corner alongside the rollout of the new Income-tax Act, 2025, in April, tax experts believe the government has an opportunity to further simplify the LTCG framework, reduce interpretational disputes and make compliance less burdensome.As Budget day approaches, Times of India Online conducted a survey asking tax experts: How can the Budget look to make the LTCG regime less complicated?Many believe the immediate priority should be smoother implementation rather than sweeping structural overhauls. At the same time, there is a clear call for further rationalisation of asset classifications, holding periods and loss set-off rules that continue to puzzle taxpayers.Let’s dive deeper into the topic and what can be expected from Budget 2026.

When LTCG is applicable as per Income tax

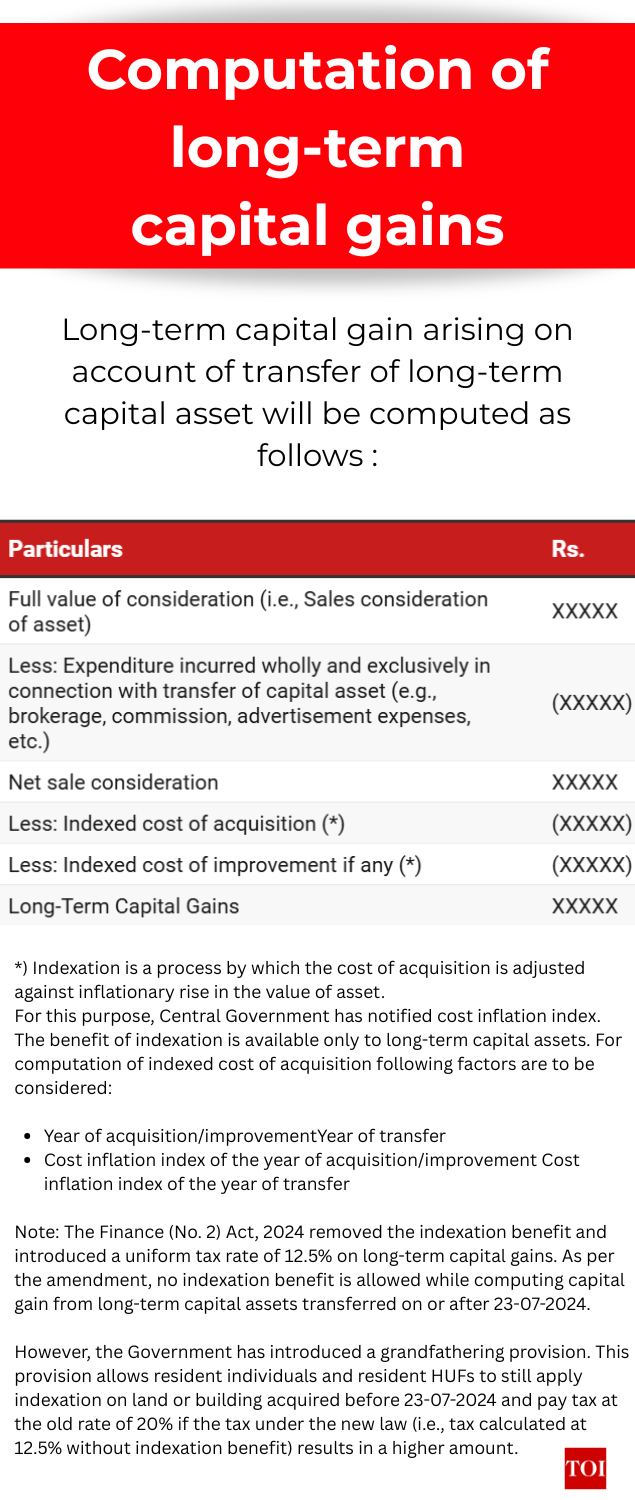

Long-term capital gain, or LTCG, refers to the profit earned when a person sells a capital asset after holding it for a specified minimum period. Capital assets include financial investments such as shares, equity mutual funds and bonds, as well as physical assets like land, houses and buildings. If the asset is held beyond the prescribed holding period, the gain is treated as long term and taxed under LTCG provisions.LTCG tax is levied on the difference between the sale price of the asset and its cost, after adjusting for certain allowable expenses and deductions.A key shift in the capital gains regime followed changes announced in Finance Bill 2024. Many long-term capital gains are now taxed at a base rate of 12.5 per cent, but the way this rate applies depends on the type of asset sold. In the case of listed equity shares, equity-oriented mutual funds, and units of business trusts, LTCG is taxed at 12.5 per cent without indexation. Only gains exceeding Rs 1.25 lakh in a financial year are taxable, and gains up to this threshold are effectively exempt, provided conditions such as payment of Securities Transaction Tax, where applicable, are met.One notable exception is when it comes to land and buildings. The Finance (No. 2) Act, 2024, removes the indexation benefit for all long-term capital assets and introduces a uniform tax rate of 12.5 per cent. However, the government has included a grandfathering provision to protect certain taxpayers. Under this provision, resident individuals and Hindu Undivided Families (HUFs) can still apply indexation on land or buildings acquired before 23 July 2024. They may choose to pay tax at the rate of 20 per cent (with grandfathering) if the tax computed under the new 12.5 per cent rate, without indexation, turns out to be higher. This move ensures that taxpayers who purchased property prior to the amendment are not disadvantaged by the LTCG framework.The holding period that determines whether a gain is long term depends on the type of asset. Whether your profit is treated as short-term or long-term depends on how long you held the asset before selling it. For sales made on or after 23 July 2024, most assets become long-term if held for more than 24 months. However, listed shares, equity-oriented mutual funds, and certain listed securities like debentures, government securities, UTI units and zero-coupon bonds qualify as long-term much earlier, after being held for more than 12 months.

Current rules applicable for FY 2025-26

For sales made before 23 July 2024, the older rules applied. Under those rules, most assets had to be held for more than 36 months to become long-term. The exceptions were the same special financial assets mentioned above, which needed only more than 12 months, and unlisted shares and immovable property (land or building), which became long-term after more than 24 months.

Focus on transition and clarity

Surabhi Marwah, Tax Partner, EY India, said the spotlight should be on easing the shift to the new law.“As the new Income-tax Act, 2025 will shortly come into effect, the focus is likely to be on ensuring a smooth transition with clear FAQs, practical guidance and easy-to-apply rules. Recent steps such as consolidating asset classes, rationalising tax rates and simplifying holding periods have already provided a strong base for streamlining the regime,” she said.“Further clarity on valuation rules and reporting, supported by pre-filled information, can ease compliance and help reduce interpretational challenges,” she added, sharing her views on the budget expectations when it comes to capital gain taxation.Too many categories, too many conditionsThe maze of asset-wise distinctions that still define how LTCG is taxed and how it can be confusing, was also raised.Sundeep Agarwal, Partner, Vialto Partners, noted that while Budget 2023 rationalised several aspects, the system remains layered. “Union Budget 2023 rationalised capital gains taxation with respect to tax rates, indexation and holding period, but some aspects of LTCG regime still remain complicated. At present, the classification of a financial asset into long-term or short-term (12 or 24 months holding period) is quite complex, it depends on multiple factors, including whether the asset is listed or unlisted or market linked, whether it is a share, mutual fund, ULIP, bond, or debenture, whether the investment is equity or debt oriented, and whether Securities Transaction Tax (STT) has been paid etc.”He further detailed various expectations from the budget to be presented this Sunday. He said, “It is expected that the FM may further simplify and standardise the assets category, thereby enhancing ease of understanding, reducing disputes, and improving overall tax compliance.”Adding his 2nd expectation, he added, “from the Budget is to simplify the provisions related to set-off of losses. Current capital gains set-off rules are governed by the classification of gains and losses into long-term or short-term. While both long-term and short-term gains can be set off against short-term losses, long-term gains can be set off only against long-term losses. Where the long-term and short-term capital gains and losses arising in the current year as well as carried forward from earlier years co-exist, then the computation becomes highly complex. Simplifying set-off rules would ease compliance and make the provisions more taxpayer-friendly.”Agarwal gave his input on the third expectation saying, “Another key expectation from the Budget concerns expanding the scope of the section 87A rebate. Currently, only the long-term capital gains from specified assets such as listed equity shares and equity-oriented mutual funds, etc., are eligible for rebate, rest other asset classes and all short-term capital gains are excluded. To ensure parity and provide meaningful relief to small taxpayers, the rebate provisions could be broadened to cover all capital gains, regardless of asset type or holding period.”

Multiple rulebooks within one regime

Radhika Viswanathan, Executive Director, Deloitte India, shed light on how different rules apply depending on the asset and the taxpayer’s profile.“LTCG has divergent rules on holding period, reinvestment relief, tax rates and computation methodology based on residential status, and nature of the underlying asset. Having multiple rulesets makes it challenging to comprehend and comply for individual taxpayers. While the last Budget addressed inconsistencies in holding periods, a further rationalisation and simplification would significantly improve ease of compliance,” she said.Further voicing his opinion on simplification of categories she said, “Greater flexibility in setting off capital losses across asset classes and the introduction of a common, simplified reinvestment relief framework together with lock-in provisions could meaningfully reduce complexity and minimise litigation. Additionally, enhanced and appropriate disclosures in Form 26AS/AIS and enabling pre-filled tax return forms that accurately capture data for LTCG would enhance voluntary compliance.”

Expectations of limited big-bang changes

Some financial experts, however, believe the government may largely stay the course after major changes in recent years.Parizad Sirwalla, Partner and Head, Global Mobility Services, Tax, KPMG in India, said, “The Finance Act (No. 2), 2024 has already rationalized capital gains tax rates and asset classifications to a large extent. Therefore, no major changes are anticipated in this area at least from an individual tax perspective.”Tanu Gupta, Partner at Mainstay Tax Advisors LLP, echoed this view while suggesting targeted relief. “The government has already undertaken substantial simplification of the capital gains framework in recent years. Key measures such as the streamlining of holding periods across asset classes (listed securities, unlisted shares, and immovable property), greater uniformity in tax rates, and the removal of indexation in certain cases have significantly reduced complexity and interpretational issues,” she said.However, she did suggest the possibility for some minor changes saying, “Given these reforms, there may be limited scope for further structural simplification of the capital gains regime at this stage. However, from a taxpayer-relief perspective, the Budget could consider a modest enhancement of the exemption threshold under section 112A. Increasing the current exemption limit of Rs 1.25 lakh on long-term capital gains from listed equity and equity-oriented funds to Rs 1.5 lakh or Rs1.75 lakh could provide incremental relief to retail investors without adding complexity to the regime.”

NRI concerns also in focus

Compliance challenges for non-resident Indians are another area flagged for attention.Richa Sawhney, Partner, Tax, Grant Thornton Bharat, said, “TDS of 1% is applicable in case of transfer of immovable property (other than agricultural land) in case of transactions exceeding INR 50 lakh, where the seller is resident India. This provision is not applicable in case the seller is a NRI. NRIs at times face a lot of delays and challenges in obtaining lower withholding certificates, during property sales. Similar provisions should be considered for NRIs as well.”

The common thread

Across views, the message to the Finance Minister was primarily less about rate cuts and more about simplifying the rulebook. Fewer asset-based distinctions, simpler loss set-off rules, broader rebates for small taxpayers and smarter pre-filled returns could turn LTCG from a technical thicket into a more navigable path for ordinary investors.Experts also shared that predictability and consistency in interpretation are just as important as tax reliefs or rate cuts. Simplified definitions, standardised reporting formats and better alignment of provisions with the tax department data could reduce disputes and confusions. The next phase of reform should make compliance feel routine rather than intimidating for the growing number of taxpayers now dealing with capital gains.